Airlines have committed to carbon-neutral growth by reducing carbon dioxide (CO2) emissions by 50% in 2050. Reducing carbon growth will require non-fossil-sourced fuels, referred to as sustainable aviation fuel (SAF)

The domestic jet fuel market size (JET A) is about 26 billion gallons per year. The global market size exceeds 81 billion gallons. Passenger demand is projected to double over the next 20 years (IATA 2016).

Airlines are very price-sensitive because jet fuel accounts for approximately 30-40% of their operating costs.

The cost of SAF production can vary widely depending on the feedstocks and production technologies used.

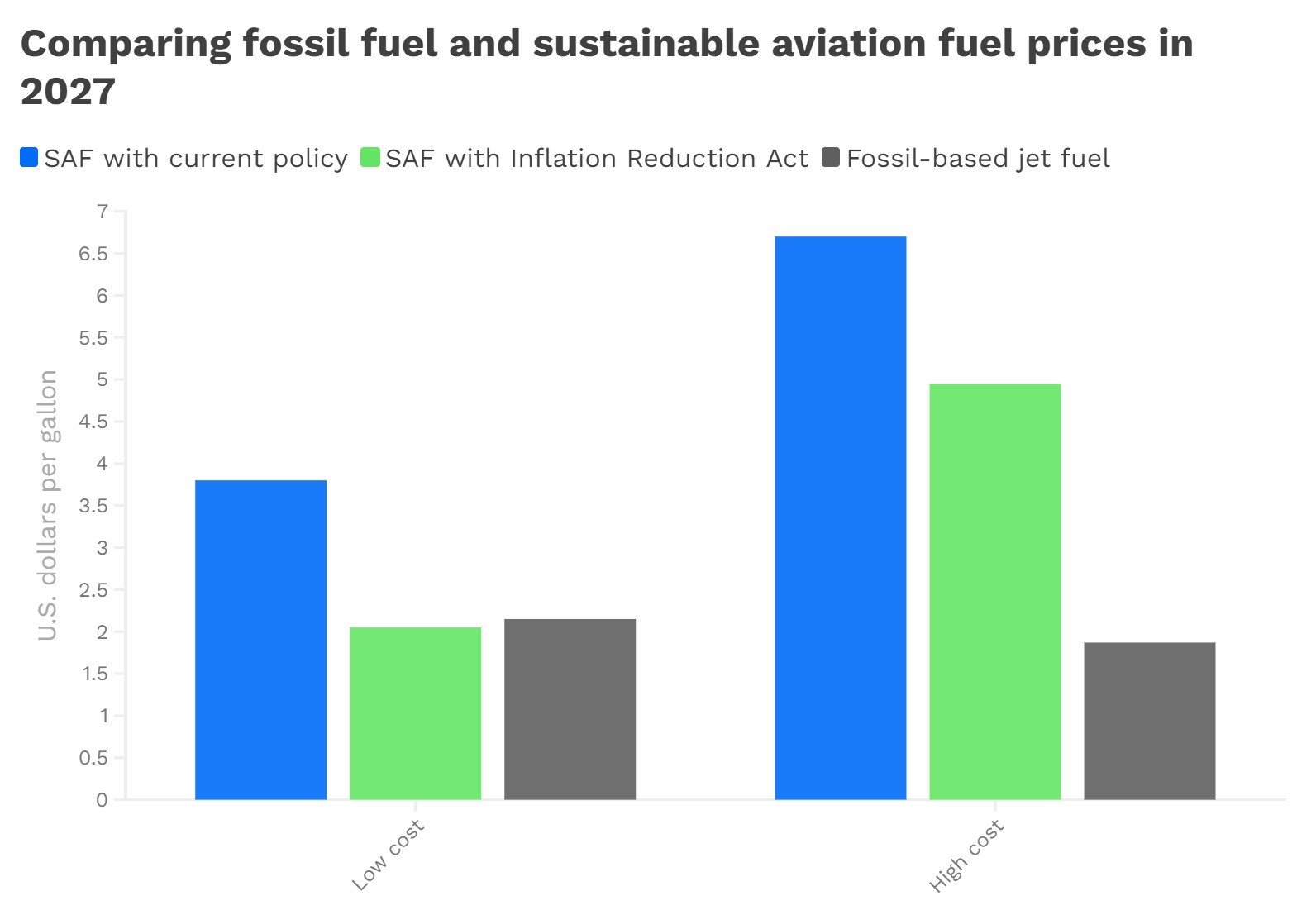

IATA estimates the cost of SAF is between two and four times higher than Jet A, although a recent announcement by Air France-KLM implied that the cost differential may be more like four to eight times the costs of kerosene.

For Air France, the way to square the circle of increased costs for using SAF is to introduce a SAF surcharge. The new fuel levy, voluntary for the moment, will see a charge of between €1 and €12 added to ticket prices depending on the flight length and the cabin class.

SAF production and use reached only 15.8 million gallons in 2022, or about 0.1 % of the fuel used by the airlines.

As of January 2019, six fuels pathways are approved as annexes to ASTM D7566 for the production of SAF:

1. Fischer-Tropsch [FT]-SPK was approved in June 2009 for up to a 50% blend with petroleum-derived jet fuel. FT-SPK is a mixture of iso- and n-alkanes derived from synthesis gas using the FT process. Syngas can be produced from reforming natural gas or from gasifying coal or biomass.

2. HEFA-SPK was approved in July 2011 for up to a 50% blend with petroleum-derived jet fuel. The molecular composition of HEFA-SPK is similar to FT-SPK, consisting of iso- and n-alkanes. The alkanes are the product of hydrotreating esters and fatty acids from fats, oils, and greases and from oilseed crops or algae.

3. SIP, hydro processed fermented sugar-synthetic iso-paraffins was approved in June 2014 for up to a 10% blend with petroleum-derived jet fuel. Unlike SPK from HEFA or FT, this is a single molecule, a 15-carbon hydrotreated sesquiterpene called farnesane, produced from fermentation of sugars. Today, the fermentation is done commercially from sugar cane juice and is used in higher-value applications, most commonly in personal care.

4. Alcohol-to-jet [ATJ]-SPK was approved in April 2016 for SPK from iso-butanol (30% blend with petroleum) and expanded in April 2018 for SPK from ethanol and for fuel blends up to 50% with petroleum. ATJ-SPK consists of iso-alkanes of 8, 12, or 16 carbons when starting from iso-butanol. The iso-alkanes are highly branched and have lower DCNs than FT or HEFA, based on data from Gevo, Inc. Sustainable Aviation Fuel: Review of Technical Pathways 20 The carbon number is broadened, and the branching level can be significantly reduced, leading to a DCN similar to FT and HEFA when starting from ethanol.

5. Applied Research Associates Catalytic Hydro thermolysis Jet, or ARA CHJ was approved in January 2020 as a 50% blend. The fuel is produced from lipids using a supercritical hydrothermal process, creating a blend stock that contains all four hydrocarbon families: n-, iso-, and cyclo-alkanes and aromatics.

6. HC-HEFA synthesized paraffinic kerosene from hydro processed hydrocarbons, esters, and fatty acids was approved in 2020 as a 10% blend. This is specifically for lipids from a B. braunii algae that have been hydrocracking/hydro isomerization to remove all oxygen and saturate double bonds. The product is rich in iso-alkanes. This is the first approval through the fast-track process.

For the purpose of this article, we will concentrate in number 2 and 4 approved pathways which we believe to have currently the most potential to scale up the SAF volume in a commercially viable way.

Benchmark Background:

Benchmark group of companies are well known for successfully developing technology and industrially scaling processes in a commercially effective manner.

Benchmark had the experience of the citrus industry, where new processes and new by-products extractions was necessary to “squeeze” more margins in a highly competitive market.

Benchmark has consistently turned down working on projects and technologies that in our view were not commercially ready.

Pathway Number 2:

Jet fuel properties fall within the light end of the diesel envelope and hence biofuels companies could sell to either market. Diesel fuel (ground transportation) is a significant competitor for lipids, including fats, oils, and greases.

Due to perceived lack of available feedstocks, SAF supporters believe that the lipid routes are not likely to meet the SAF volume demand.

However, the step up from biodiesel to SAF is simple, requiring only further refining and cleaning.

A hydrotreating process could be included to help eliminate impurities, reduce the oxygen and increase the energy content (5-10% more) to match the energy content of petroleum diesel.

We believe the feedstock supply can be augmented by promoting high oil rotational, non-human crops that can provide the lipids required. Sample of these crops include Camelina (mustard seeds), Hemps, Pennycress and others. Even the lipids of algae can be utilized to manufacture SAF.

As an example, 37,750 acres of Camelina (In a rotation program with grain sorghum) can provide enough oil to feed a 10 million gallons of SAF per year plant.

Benchmark owns a patent for removing oil from fibrous material that has proven very effective across different processes and applications. We are confident that by promoting cultivation of rotational crops we can industrially extract the lipids necessary for a biodiesel-SAF plant.

We estimate that SAF cost per gallon utilizing Pathway 2 can be commercially competitive with JET A fuel.

Pathway Number 4 - Alcohol to JET Fuels (ETJ)

We continue to review the potential different technologies available to convert fuel ethanol into SAF.

However, thus far, there are costs that need to be managed to commercially develop an SAF processing plant utilizing fuel ethanol as a feedstock.

Amongst factors of production difficult to control we find:

High Energy requirements to produce the Syngas. As an example, there is demand of 90 MW of electricity on a 10 MGY ethanol to SAF plant.

High CAPEX on the Syngas Plant in addition to the CAPEX to produce ethanol.

Use of renewable green hydrogen anticipated.

Expensive rare metals are required for the reformers that will have a limited useful life and will need frequent replacement.

Technical challenges in fuel conversion: The conversion of ethanol to jet fuel requires a complex series of chemical reactions that can be challenging to optimize. One potential issue is the formation of unwanted byproducts during the conversion process, which can reduce the overall efficiency of the process, ethanol to SAF yield and increase emissions.

Cost competitiveness: The production cost of ethanol-based jet fuel is currently higher than conventional jet fuel. The cost of production remains higher due to the complexity of the fuel conversion process.

Proponents of the ethanol to jet fuel pathway generally include the utilization of “Green Hydrogen” to reduce the carbon score in the production of SAF.

Green hydrogen is produced from the electrolysis of water using renewable electricity, such as solar or wind power, and is considered a promising pathway for decarbonizing the energy sector. However, there are some potential shortcomings associated with the production of green hydrogen:

High cost: The production of green hydrogen can be expensive due to the high capital costs associated with building and operating large-scale electrolysis facilities, as well as the cost of renewable electricity. This can make green hydrogen less competitive than conventional hydrogen produced from fossil fuels.

Energy requirements: The production of green hydrogen requires a significant amount of renewable energy, which can be challenging to produce in sufficient quantities, especially during periods of low renewable energy generation. This may require the installation of additional renewable energy capacity or energy storage systems to ensure a reliable supply of green hydrogen.

Water use: The production of green hydrogen requires a large amount of water, and in some regions, water scarcity may be a constraint on the scalability of green hydrogen production. However, the use of wastewater or seawater for electrolysis can help to mitigate this issue.

Production scale: The production of green hydrogen is currently limited by the availability of renewable electricity, as well as the availability of water and electrolysis equipment. Scaling up green hydrogen production to meet the needs of SAF production will require significant investment and infrastructure development.

Supply chain challenges: The production and distribution of green hydrogen will require the development of new infrastructure, such as hydrogen storage and transport systems. This can be challenging and costly, especially in regions with limited existing infrastructure.

Benchmark is currently evaluating green hydrogen for the production of renewable fertilizer (Ammonia).

A competitive comparison of SAF vs. JET A utilizing projected revenues between a fuel ethanol plant vs. utilizing the ethanol as a feedstock for JET A / SAF will look as follows:

Note: Platts reported the retail price of SAF during Q4, 2022 in California at $8.28 per gallon. SAF Tax Credit according to new Inflation Reduction Act legislation.

From the above analysis, one can conclude that currently there is not enough of a step up in revenues when utilizing ethanol to SAF, to support commercially competing with JET A.

Overall, the ethanol to jet fuel pathway has the potential to be a promising pathway for the production of SAF, but there are shortcomings that must be addressed in order to ensure that this pathway can be implemented in a sustainable and cost-effective manner.

We continue investigating the different SAF pathways, however we need more testing including developing new production processes (utilization of super-heated steam) to affect a breakthrough in the costs of SAF production.

For additional information, please contact the company.